Term Life Insurance

Rules of thumb and online calculators

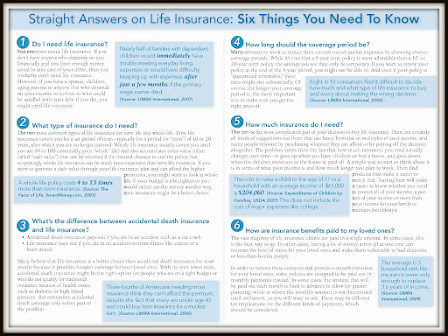

So, how much term life insurance do you really need? Start with one of the general guidelines to get an idea. A commonly quoted estimate is 7-10 times your current annual salary. So, if you make $40,000 a year, you'd be looking at a $200,000 to $400,000 policy. For greater payoff, MSN Money notes two other guidelines: 17 times your annual salary or a sliding scale based on your age.

While these guidelines are a good starting place, financial advisers are quick to dismiss rules of thumb as too narrow because they don't take into account your specific needs. Online calculators allow you to customize your estimate by asking not only for your salary, but debt obligations, number and ages of children, and more.

Here are a couple:

- The LIFE Foundation Life Insurance Needs Calculator

- MSN Money Life Insurance Needs Estimator

Online calculators have drawbacks, however. They don't offer options for nontraditional families, so it can be confusing to determine what data to include for your particular situation. Calculators can be skimpy with explanations of the terms they use or how the final figures are reached.

Term life insurance buys peace of mind that your dependents will live on solid financial ground if you die prematurely and can no longer provide for them.

But many consumers get confused and make term life insurance mistakes that put their families at risk. Here are four myths about term life and what you should know:

1. I don't need life insurance because I'm a stay-at-home parent

Even if you don't earn an income, your death will pack a financial wallop because your family will have to pay for all those services you provide for free, such as child care. You should also consider your future earning potential in case you return to the workforce, as many stay-at-home parents do once their kids are in school.

2. I can use a formula to figure out how much life insurance to buy

Popular formulas, such as multiplying your income by a certain number, are too simplistic. A thorough needs assessment is in order. Evaluate short-term and long-term needs and your current financial resources. To determine the length of the term, review your debts, and the financial needs of your dependents and when those will change.

3. I can't qualify for life insurance because I had a serious illness

Don't automatically count yourself out for coverage. With treatment advances and better patient outcomes, life insurance companies have changed their underwriting guidelines for many diseases and conditions. For instance, today it's much easier to qualify for coverage at decent life insurance rates even if you've been treated for breast cancer, prostate cancer or depression.

4. I don't need to buy individual life insurance because I have coverage through work

Group life insurance at your job is a terrific benefit, but the coverage typically isn't enough for most people. Check the level of group coverage, evaluate your needs and buy additional insurance if necessary to protect your family.

Besides comparing life insurance quotes, talk to us today to design the best life insurance plan for your family.